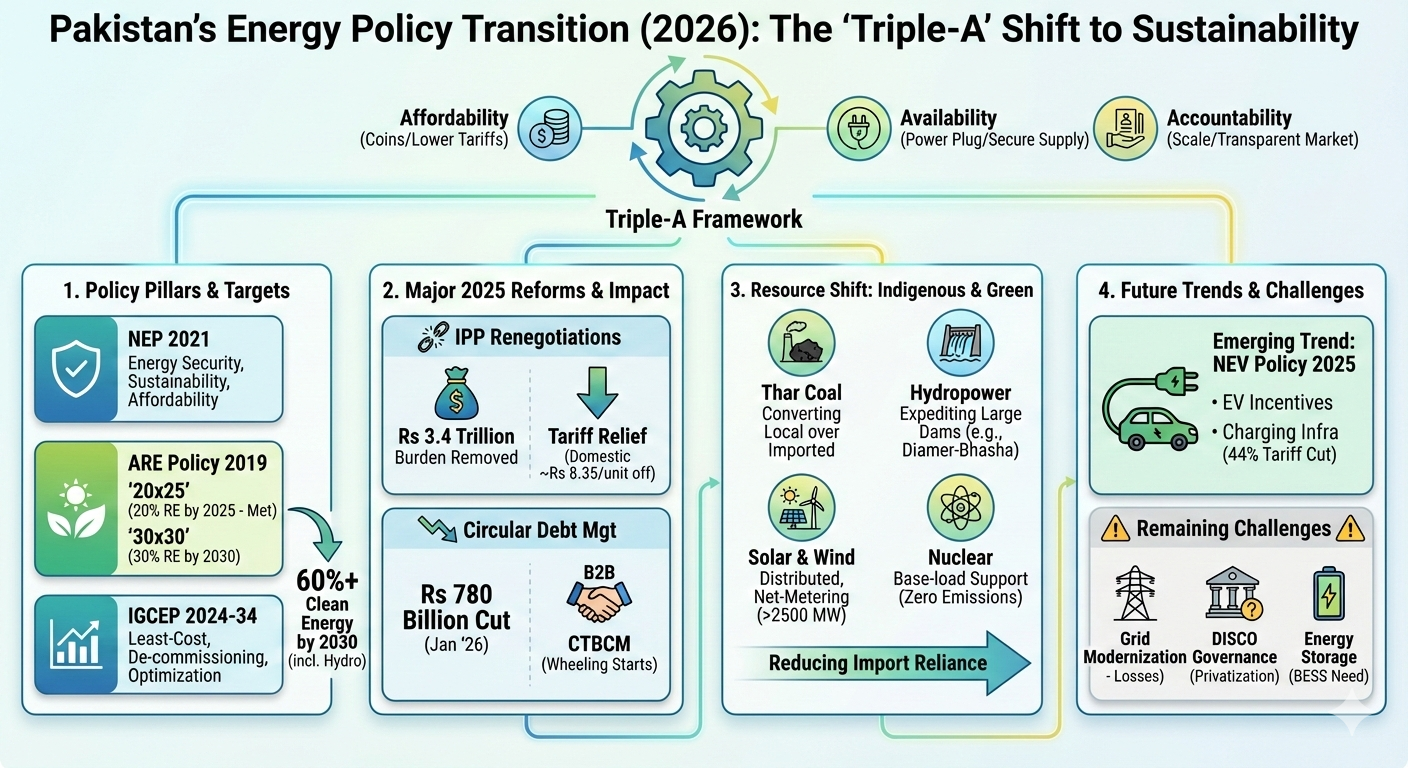

A Review of Pakistan’Pakistan’s energy landscape is undergoing a monumental shift. As of early 2026, the country is moving away from its historical reliance on expensive imported fossil fuels toward a more sustainable, indigenous, and market-driven “Triple-A” framework: Affordability, Availability, and Accountability.

This review analyzes the core components of Pakistan’s energy policies, the recent structural reforms of 2025, and the roadmap for 2030.

1. Key Pillars of Pakistan’s Energy Policy

The current policy framework is governed by three primary documents that set the strategic direction for the power sector.

A. National Electricity Policy (NEP) 2021

The NEP 2021 serves as the “constitution” for the power sector. It prioritizes:

- Energy Security: Reducing dependence on imported fuel (LNG and Furnace Oil).

- Sustainability: Increasing the share of “green” energy.

- Affordability: Rationalizing tariffs to support industrial growth and domestic relief.

B. Alternative & Renewable Energy (ARE) Policy 2019

The ARE Policy is the cornerstone of Pakistan’s green transition. It set ambitious “20×25” and “30×30” targets:

- Target 1: 20% of generation capacity from renewables by 2025 (largely met through solar and wind).

- Target 2: 30% of generation capacity from renewables by 2030 (excluding large hydel).

When combined with hydropower, Pakistan aims for over 60% clean energy by 2030.

C. IGCEP 2024–2034 (Integrated Generation Capacity Expansion Plan)

Approved in May 2025, the revised IGCEP is a 10-year data-driven roadmap. It focuses on:

- Least-Cost Principle: Only the most cost-effective projects are allowed to enter the grid.

- De-commissioning: Shutting down inefficient, high-heat-rate thermal plants.

- Optimization: Excluding nearly 8,000 MW of high-cost projects to save the national exchequer approximately $17 billion over the next decade.

2. Major Reforms and 2025 Performance Review

The year 2025 was a “Year of Correction” for Pakistan’s energy sector. The government initiated aggressive measures to stabilize the economy.

IPP Renegotiations and Savings

In a historic move during late 2025, the government renegotiated contracts with several Independent Power Producers (IPPs).

- Financial Impact: Eliminated a cumulative burden of Rs 3.4 trillion.

- Tariff Relief: Reduced electricity prices by approximately Rs 8.35 per unit for domestic users and up to Rs 16.68 per unit for industrial consumers.

Circular Debt Management

Circular debt has long been the “Achilles’ heel” of the sector. By January 2026:

- The government reduced circular debt by Rs 780 billion through improved recoveries and financial discipline.

- A shift toward the Competitive Trading Bilateral Contract Market (CTBCM) has begun, allowing private B2B power sales (Wheeling), which reduces the government’s role as the sole purchaser.

3. The Shift to Indigenous Resources

To protect the economy from global oil price volatility, Pakistan is pivoting toward local resources:

| Resource Type | Policy Focus | Current Status (2026) |

| Thar Coal | Transition from imported coal to indigenous Thar Coal. | Major conversion projects for existing plants are underway. |

| Hydropower | Large-scale projects like Diamer-Bhasha and Mohmand Dams. | Construction expedited to meet 2030 targets. |

| Solar & Wind | Distributed generation and solarization of tube wells. | Net-metering capacity has surpassed 2,500 MW. |

| Nuclear | Base-load support with zero emissions. | Contributing roughly 8-10% to the national grid. |

4. Emerging Trends: Electric Vehicles & Efficiency

The New Energy Vehicles (NEV) Policy 2025 is the latest addition to the policy suite. It aims to:

- Lower the oil import bill by incentivizing electric 2-wheelers and 3-wheelers.

- Provide a 44% tariff reduction for EV charging stations to encourage infrastructure growth.

- Establish a “New Energy Vehicle Center” to regulate safety and performance standards.

Expert Insight: “Pakistan is no longer just adding capacity; it is optimizing the energy mix. The focus has shifted from ‘MW at any cost’ to ‘Affordable MW for the consumer’.”

5. Challenges Remaining in 2026

Despite the progress, several hurdles remain:

- Transmission Losses: The aging NTDC grid requires modernization to handle the intermittent nature of solar and wind.

- Governance in DISCOs: High “Technical and Commercial” (T&C) losses in certain regions remain a drain. The government has initiated the privatization of three DISCOs in 2025 to address this.

- Energy Storage: As solarization grows, the need for large-scale battery storage solutions (BESS) is becoming critical for grid stability.

Useful External Links

Alternative Energy Development Board (AEDB)s Energy Policies